List of Assets, Liabilities, and Equity with Examples

The list of assets, liabilities, and equity is useful for every business as it outlines all the company owns, all that it owes, and all that has been invested in the business by shareholders or owners. Companies usually keep records of their finances using a combination of the balance sheet, statement of cash flows, and income statement. These financial statements are useful in tracking income, expenditures, and other financial transactions that occur in a company.

Among these three financial statements, it is the balance sheet that clearly outlines the list of a company’s assets, liabilities, and equity. The balance sheet is governed by the accounting equation, Assets = Liabilities + Equity. This means that the total sum of a company’s assets should always be equal to the sum of its liabilities and equity if the company’s financials are done properly and balanced.

In a situation where the company’s assets are not equal to the sum of its liabilities and equity, it means that there is a problem with the company’s accounting.

This can occur from improper record keeping of the various journal entries that record company transactions. Before we discuss the list of assets, liabilities, and equity of a company, let us understand each term.

See also: Are expenses assets, liabilities, or equity?

What are assets, liabilities, and equity?

Understanding assets, liabilities, and equity

Assets refer to resource whether tangible or intangible which is owned by a company and adds value to it. These resources generally bring present or future benefits to the company by easing operations, reducing cash outflows, or increasing cash inflows. This often includes land, machinery, buildings, cash, etc. Assets aid a company to increase its equity while they meet its commitments.

Liabilities refer to the company’s obligations to creditors or suppliers which they need to fulfill in the short-term or long-term. This includes money the company needs to repay or goods and services they need to supply or render respectively. These obligations are usually settled using the company’s assets and typically arise from past transactions.

Equity refers to a combination of what the company has left over after it has subtracted all that it owes from all that it owns, that is, the difference between a company’s total assets and its total liabilities, is its equity. Oftentimes, these may also include investments into the business by the business owners or other investors through the purchase of shares.

The balance sheet which records the assets, liabilities, and equity of a company is sometimes referred to as a statement of net worth or a statement of financial position. This is because it summarizes the financial position of a firm at a glance, showing all the assets, liabilities, and equity.

See also: Are Expenses Liabilities on a Balance Sheet?

What are 10 examples of assets?

What are 5 examples of liabilities?

What are some examples of equity?

See also: Is revenue an asset or equity?

Examples of assets, liabilities, and equity

- Assets

- Liabilities

- Equity

Examples of assets

Assets are usually divided into two depending on the ease with which they may be converted into cash. Current or short-term assets are resources that can be converted into cash in a fiscal year or given operating cycle. Common examples of current assets include cash and cash equivalents, marketable short-term investments in securities such as government bonds or treasury bills, inventories, notes receivable, prepaid expenses, and accounts receivable.

Inventories record the products that the company has for sale. Monies owed to the company which contains interest payments in addition to the main balance are notes receivable. Accounts receivable is an asset account that comprises money owed to the company by its clients. Prepaid expenses are payments made in advance for products or services such as insurance, electricity, cable tv, and internet.

Non-current or fixed assets are resources that will bring economic benefit to the company in the long run and generally require more than one fiscal year to get converted into cash. Common examples of fixed assets include property, plant, equipment, intellectual property, vehicles, patents, goodwill, copyright, machinery, trademarks, furniture, and land.

Examples of liabilities

Liabilities are also classified into three based on how the liability arises. The first is short-term or current liabilities which are obligations that must be settled within 12 months. Common examples of current liabilities include unearned revenue, and recurring operational expenses such as salaries, rent, electricity, and other utility bills. It also includes accounts payable, dividends payable, notes payable, interest payments, and other short-term loans as well as taxes such as sales, payroll, income, and investment taxes.

Unearned revenue refers to the revenue paid in advance by clients for products or services which they are yet to receive. Accounts payable is the sum owed by the company to its creditors or suppliers. Dividend payable refers to distributions that will be made to shareholders as a dividend on their investment in the company.

Non-current or long-term liabilities generally require over a fiscal year for repayment. Common examples of long-term liabilities include capital leases, bonds payable, pension payments, debentures, mortgages, and deferred taxes.

Contingent liabilities are liabilities that may result based on the outcome of a future event such as the outcome of a lawsuit, injuries from product use, or honoring product warranties. Common examples of contingent liabilities include non-operating, legal, product, and warranty liabilities.

Examples of equity

Equity is a combination of all capital that has been directly invested into the venture by its founders as well as capital from the sale of shares and reinvested income.

Common examples of equity include retained earnings, paid-in capital, and share capital. Retained earnings refer to the portion of a company’s profits that have been retained for future use as opposed to being paid out as dividends. Paid-in capital refers to the excess amount realized from the sale of shares above their par value. Share capital is the sum realized from stock sale at its par value.

Which financial statement lists all assets, liabilities, and owner’s equity?

See also: Is accumulated depreciation a fixed asset?

List of assets, liabilities, and equity (Classification)

- List of assets

- List of liabilities

- List of equity

Let us have a look at a list of assets, liabilities, and equity that a company may have.

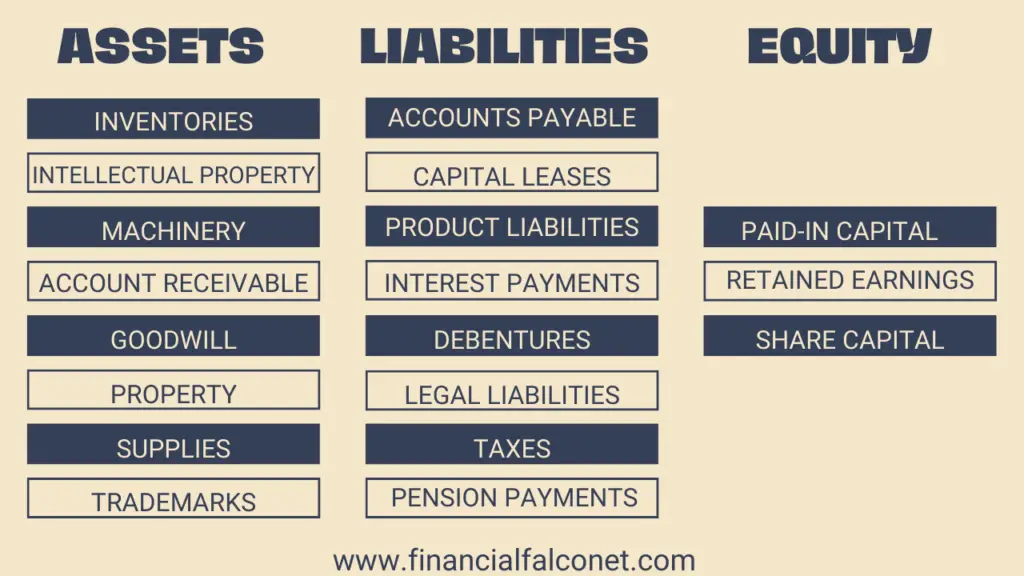

List of assets

- Current assets

- Intangible assets

- Fixed assets

Current assets

- Notes receivable

- Cash and cash equivalents

- Supplies

- Marketable short-term investments in securities e.g government bonds and treasury bills.

- Inventories

- Prepaid expenses e.g insurance, salary advance, electricity, cable tv, and internet.

- Account receivable

Intangible assets

- Patents

- Intellectual property

- Goodwill

- Copyright

- Trademarks

Fixed assets

- Property

- Plant

- Equipment

- Vehicles

- Machinery

- Land

- Fixtures and furniture

List of liabilities

- Short-term liabilities

- Contingent liabilities

- Long-term liabilities

Short-term liabilities

- Recurring operational expenses e.g salaries, rent, electricity, and other utility bills.

- Accounts payable

- Current portion of long-term debt

- Notes payable

- Unearned revenue

- Interest payments

- Other accrued expenses

- Short-term loans

- Taxes e.g sales, payroll, income, and investment taxes.

Contingent liabilities

- Non-operating liabilities

- Legal liabilities

- Product liabilities

- Warranty liabilities

Long-term liabilities

- Capital leases

- Bonds payable

- Pension payments

- Debentures

- Mortgages

- Deferred taxes

List of equity

- Retained earnings

- Paid-in capital

- Share capital

See also: Service Revenue Asset or Liability?

What accounts are assets, liabilities, and equity?

Conclusion

The list of assets, liabilities, and equity are the largest classifications found in a company’s spreadsheet and is the foundation for its balance sheet. Every account in the company books that records transactions usually falls under either of these three categories. As such, adequate and proper record-keeping is the bedrock of having a statement of financial position that is devoid of errors and provides the right information about a company’s financial standing.