Net Income vs Net Revenue Differences and Similarities

Investors and analysts compare net income vs net revenue to assess a company’s financial stability and profitability. It is important to note that these terms are not interchangeable, they vary, and to understand their differences, one has to understand the income statement. In this article, we see what is net income, net revenue, net income vs net revenue differences, and their similarities.

See also: Income Statement Ratios Formulas and Examples

What is net income?

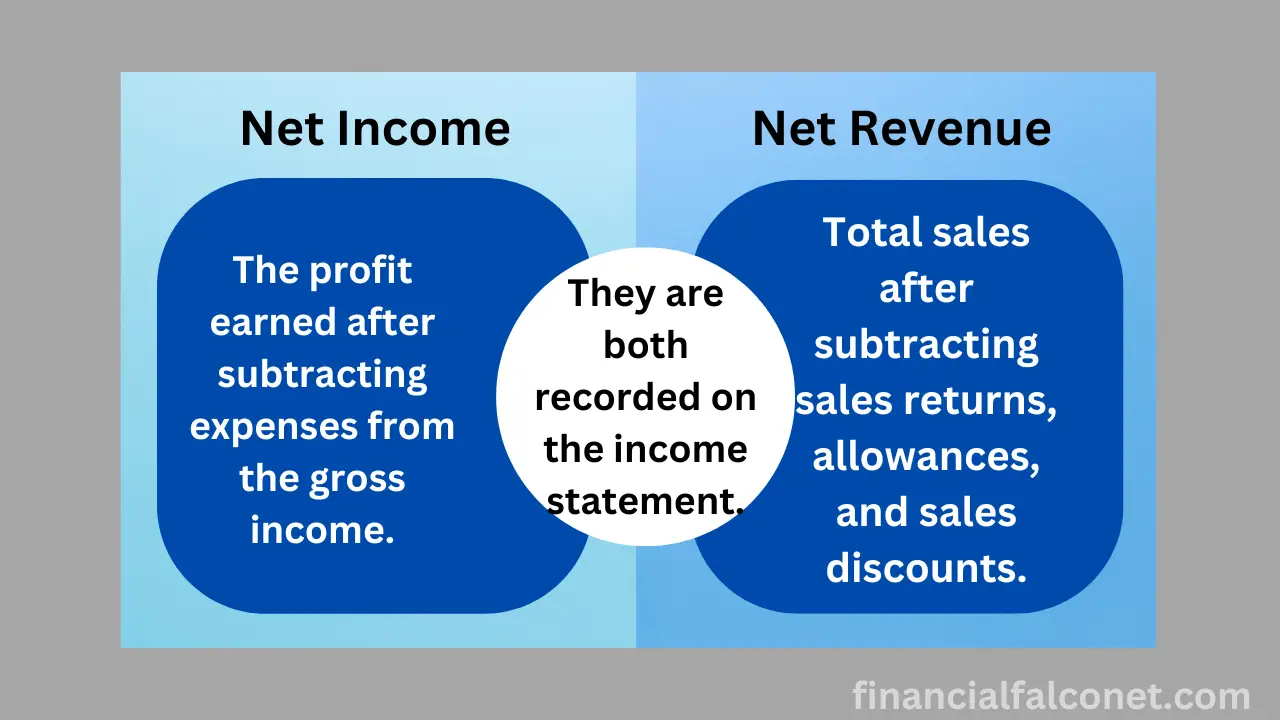

When a company’s net revenue is taken and expenses are subtracted, the taxable income will be left. The amount left after determining the amount of tax owed and subtracting it from the taxable income is the net profit or net income.

Net income appears as the last item on the income statement and for this, it is referred to as the bottom line. This value clearly tells whether a business is profitable or not and for this, it is a very important metric for any business. It is the most looked-after figure in a company’s financial statements.

The net income figure has an impact on a lot of financial ratios, particularly the profitability ratios. Shareholders take a close look at this figure as the dividend paid to shareholders is wholly dependent on the net income of a company. Lower net income may result from a number of factors such as poor sales, poor management, and high expenses.

Net income varies across companies and industries which can be due to the size of the company and the industry in which it works. Some companies have heavy asset business models and for this, the depreciation expenses will be high, while others may have light asset models. Furthermore, growth factors in industries, debt levels, and government taxes have an impact on the net income figures of a company.

Although net income is an important metric when it comes to the profit earned by the company, it is not the actual cash that the company earns. The company’s income statement includes many non-cash items such as depreciation and amortization. With this, any change that occurs in the net income or the financial ratios impacted by it should be properly analyzed.

In other words, although net income is commonly used as a measure of a company’s performance, it is bound to yield misleading results under circumstances such as cash flows. Cash flow is different from net income since the net income calculation or analysis includes noncash revenue and expenses and revenues. Therefore, net income that is derived under the cash basis accounting will differ substantially from the one derived under the accrual basis of accounting. This is because the first method is based on cash transactions while the second records transactions regardless of the changes in cash flows. Accrual accounting is acceptable by the generally accepted accounting principles (GAAP).

Another factor that can cause the net income figure to be quite misleading is fraudulent and aggressive accounting practices as this can lead to a net income that is unusually large. This will certainly not reflect the true underlying profitability of the business.

Therefore, an undue focus on the net income figure can bring about other problems in a company such as excessive use of working capital, a decline in cash balances, obsolete inventory, heavy debt usage, etc. With this, it is generally best to rely on net income information only in conjunction with other types of information or more preferably only after the financial statements have been audited.

What is net revenue?

Many businesses purchase discounts in order to encourage customers to buy their products and services, especially in the retail and wholesale sectors. Also, they use purchase allowances to encourage buyers who purchase goods or services on credit to pay their balances sooner.

So, when a company provides a discount or an allowance to a customer, it appears on the income statement as a reduction that occurs in revenue. This implies that the net revenue is the actual revenue of a company for the specified period.

So, for every income statement, the top line is the gross revenue, which is the amount of money that the company has generated before taking out anything. The net revenue now becomes the amount of gross revenue that is left over after deducting costs and losses, and it is used to pay for the operations of a business or the cost of production.

The difference between a business’s gross revenue figures and that of the net revenue indicates how well its marketing and sales methods are working. In this case, a large discount may be an indication that a business initially priced the products too high.

See also: Unearned Revenue is What Type of Account?

Net income vs net revenue differences

- The main difference between net income and net revenue is that net income comprises the difference between the net revenue and expenses while net revenue is the difference between a company’s gross revenue and sales returns, allowances, and sales discounts.

- Net income is the last item on the income statement while net revenue is usually the third item on the income statement, and the top line is usually the gross sales/revenue.

- The calculation of net income is usually dependent on the net revenue while net revenue is totally dependent on the gross revenue.

- While net income is the subset of the net revenue, the net revenue is the superset of the net income.

- Net revenue is always greater than the net income while the net income is always less than the net revenue. It would be abnormal for this trend to be violated.

Differences between net income and net revenue: comparison table

| Basis for comparison | Net income | Net revenue |

|---|---|---|

| Meaning | The profit earned by a business after deducting all the expenses from the net sales. | The total sales made by a company after deducting all the sales returns, allowances, and discounts from the gross sales. |

| Position in an income statement | It is always the last line item in an income statement. | Usually, the third item listed at the top of the income statement. |

| Dependence | Net income totally depends on the net revenue, meaning that without revenue generally, there can be a net loss. Without net revenue, it is impossible to compute net income. | Since net revenue appears first, it is not dependent on the net income |

| Subset | Usually the subset of net revenue. | The superset of net income. |

| More or less | Net income is usually less than net revenue. | Net revenue is usually greater than net income since the calculation of the latter depends on the former. |

| Uses | The payment of dividends as well as the amount of a company’s retained earnings is usually dependent on the net income. | Used in further calculating the net income. |

Understanding the income statement will aid in understanding the differences between net revenue and net income. There may be cases whereby a company will have no net income despite the fact that it earned revenue (net). To be more realistic, if the amount of the net revenue is equal to the amount of expenses incurred, there will be no net income and if the amount of expenses exceeds that of the net revenue, it will be regarded as a net loss.

Net income vs net revenue similarities

- The net income and the net revenue are both recorded on a company’s income statement.

- They are both used in demonstrating or assessing a firm’s financial stability and profitability.

- The two components tend to represent cash availability in the business.

See also: Bad Debt Expense on Income statement